.png)

.jpg)

For this final edition of the year, I’m sharing the major changes that took place in 2024, sometimes illustrated with graphs.

In 2024, we continued to see models evolve and become increasingly powerful. All tech giants now have their own model, but none truly stands out in terms of performance.

There’s a kind of commoditization of LLMs: more or less, they’re all roughly equivalent. As a result, companies tend to adopt models from their existing ecosystem (Microsoft, Google, etc.), while individuals prefer models that are easy to use, with comprehensive interfaces (like ChatGPT, Claude, etc.).

➔ In B2B, the distribution is more heterogeneous.

➔ In B2C, OpenAI still dominates overwhelmingly (over 50%).

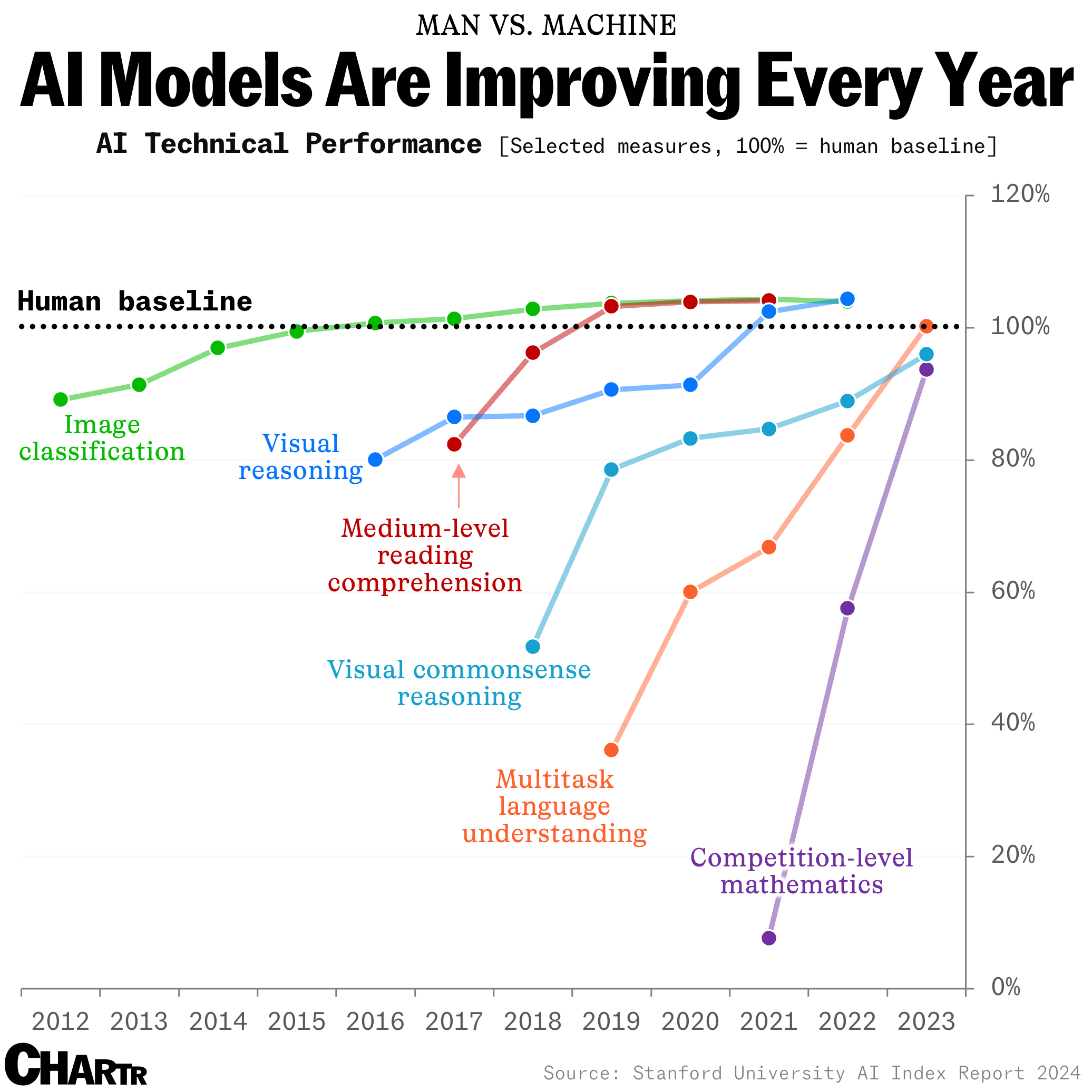

In 2023, humans could still compete with AI on certain tasks, as this chart showed.

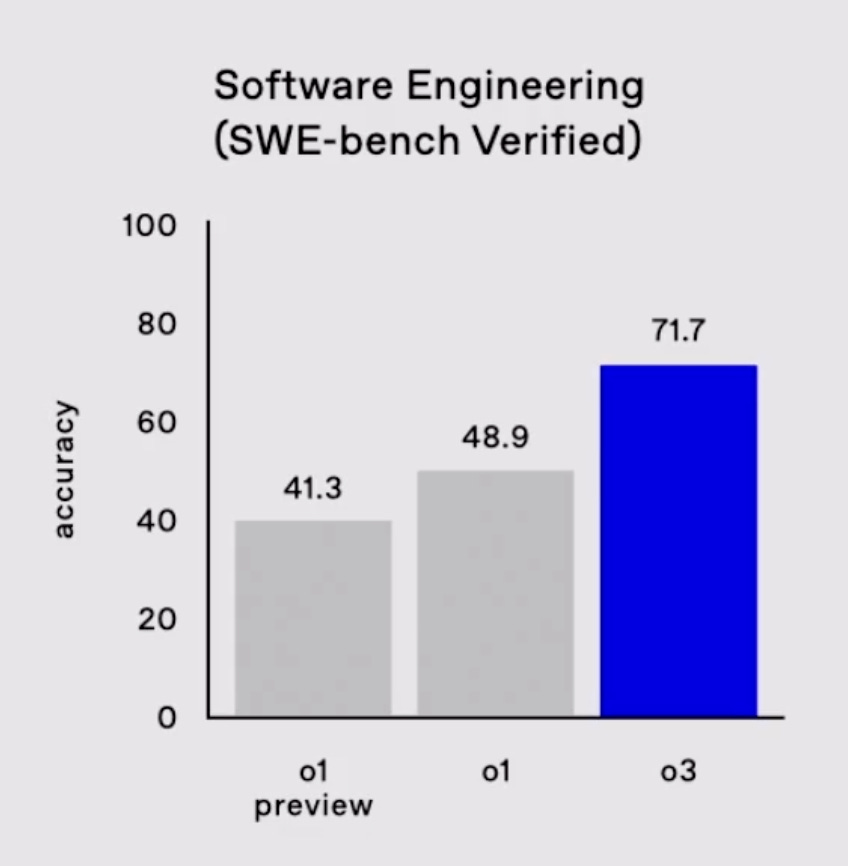

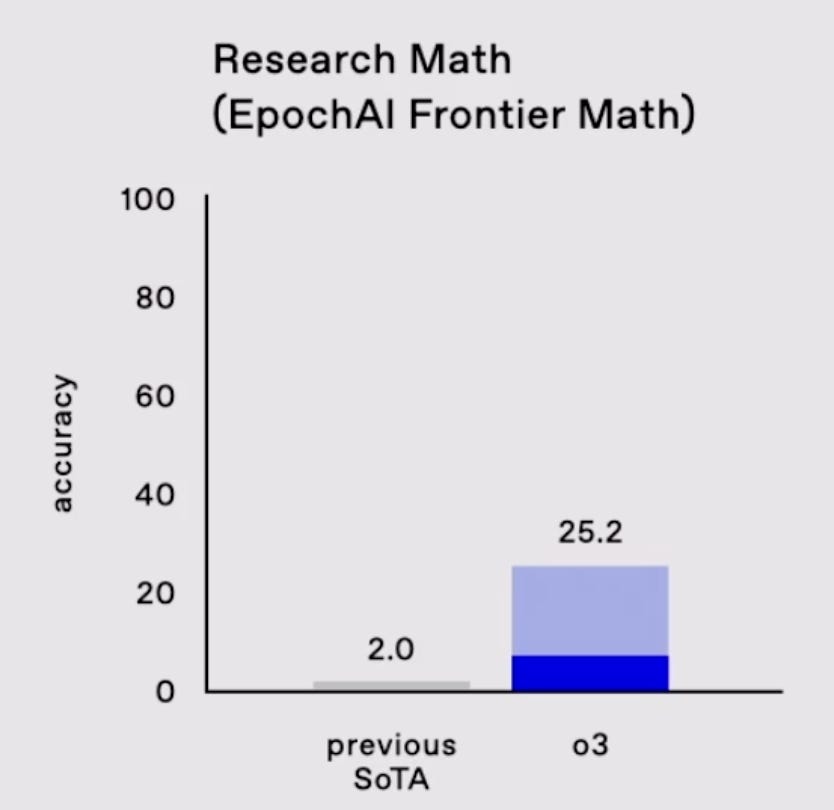

In 2024, AI models have completely crushed the benchmarks, which are now hardly relevant to measure progress.

Here are two concrete examples:

This shows significant breakthroughs, even if there’s talk of a performance plateau.

Yes, some 2024 model releases were less groundbreaking than the GPT-3.5 → GPT-4 jump, but recent improvements show the ceiling hasn't been hit yet. It may be the benchmarks that are becoming outdated.

Companies keep improving models to make them:

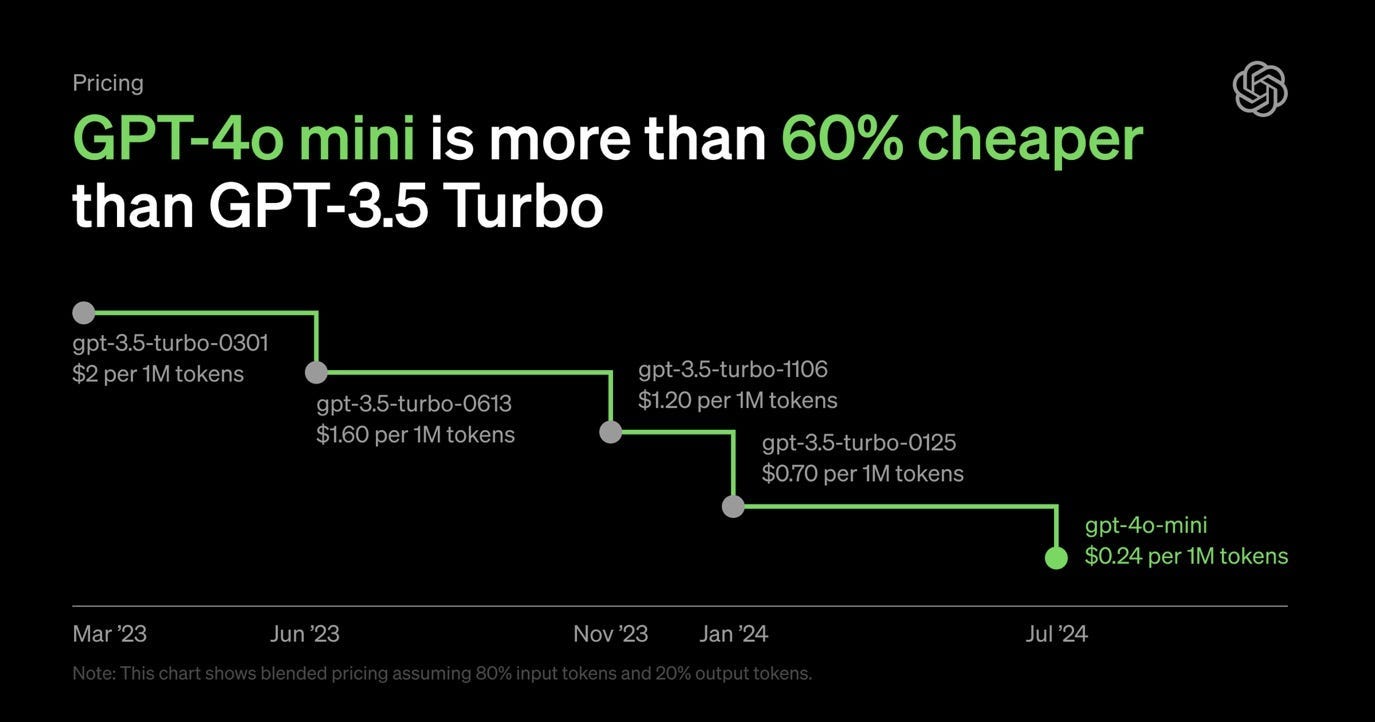

On that last point: the cost of models dropped significantly, unlocking more use cases.

This graph stops at July 2024 and doesn’t reflect changes like:

However, data quality remains a major challenge.

➔ If data is poor (“garbage in”), especially when scraped from the internet, the output will be equally poor (“garbage out”).

2024 brought a major shift: AI features were added everywhere, across all tools and services.

There’s no point listing where AI was added — it’s everywhere!

Often added as a new layer, it boosts the tool without fundamentally transforming it.

➔ Most tools haven’t been reinvented — just enhanced by AI.

Example: search.

Google is rolling out AI Overviews to summarize search results. But it’s a gradual rollout, with mixed success — as seen in recent controversies.

This gradual deployment is a real opportunity for new players to start from scratch and solve existing problems better.

That’s the idea behind the verticalization of AI.

As mentioned in a recent newsletter, Perplexity is one such serious player when it comes to rethinking online search.

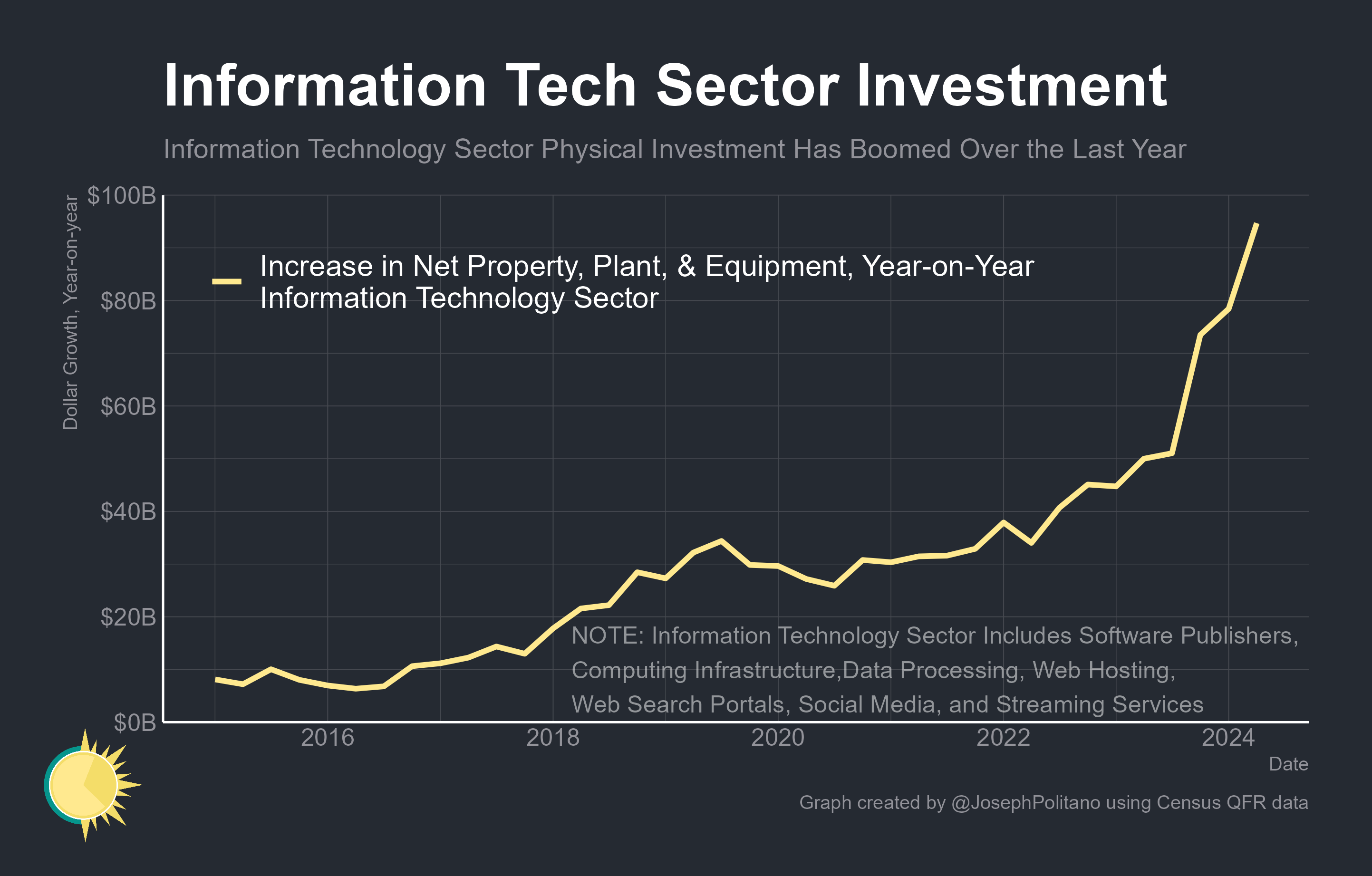

Tech investment is booming — and this graph is just the beginning. It illustrates the coming impact:

All major tech companies (Meta, Microsoft, Amazon, Google) are pouring billions into physical infrastructure.

For example:

➔ Meta invested $15.2B in the first half of 2024 alone.

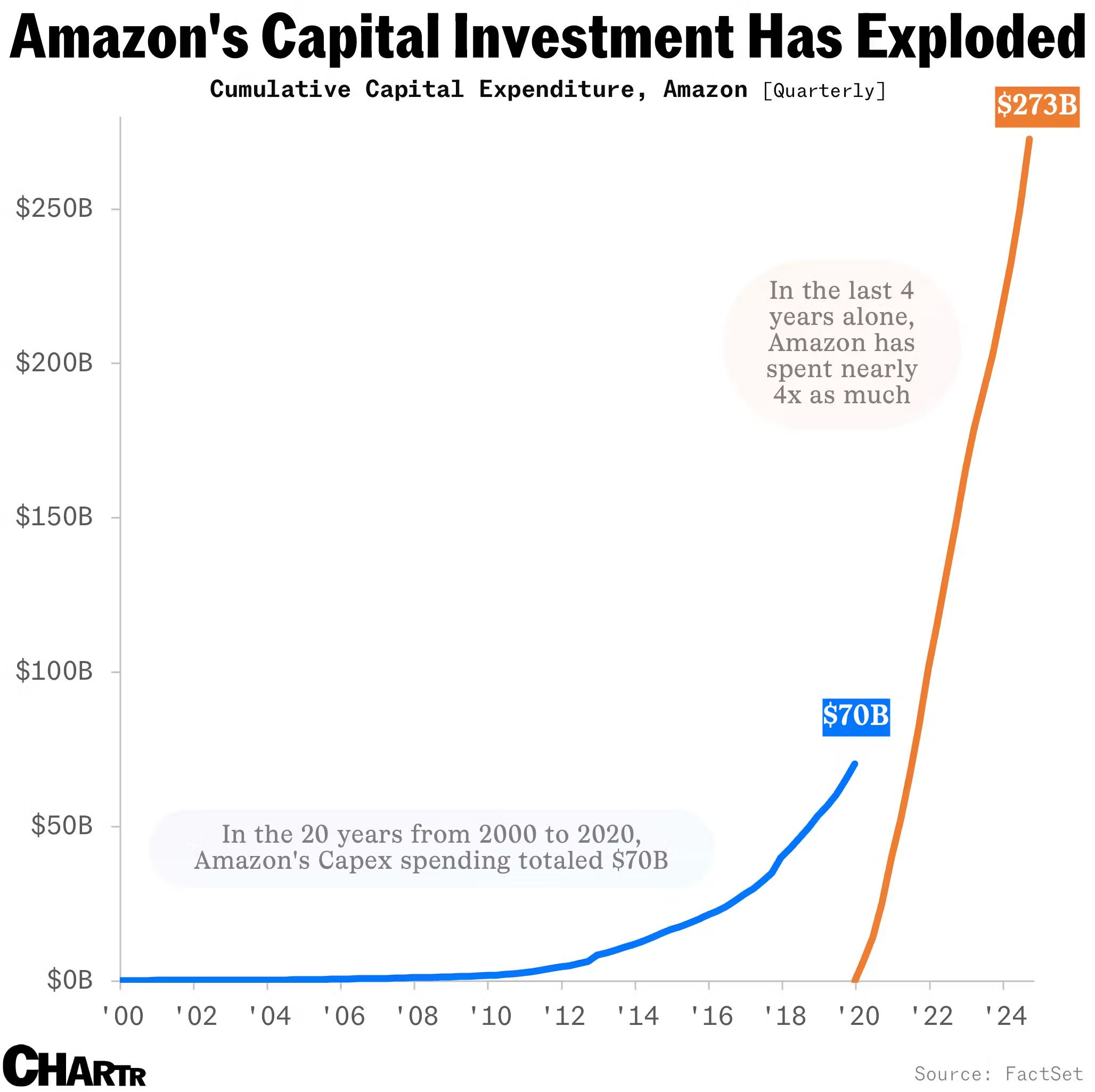

➔ Amazon spent $273B over four years to stay in the AI race — mostly infrastructure.

For comparison:

➔ Amazon spent only $70B between 2000 and 2020.

They’ve multiplied that by 4 in just a quarter of the time.

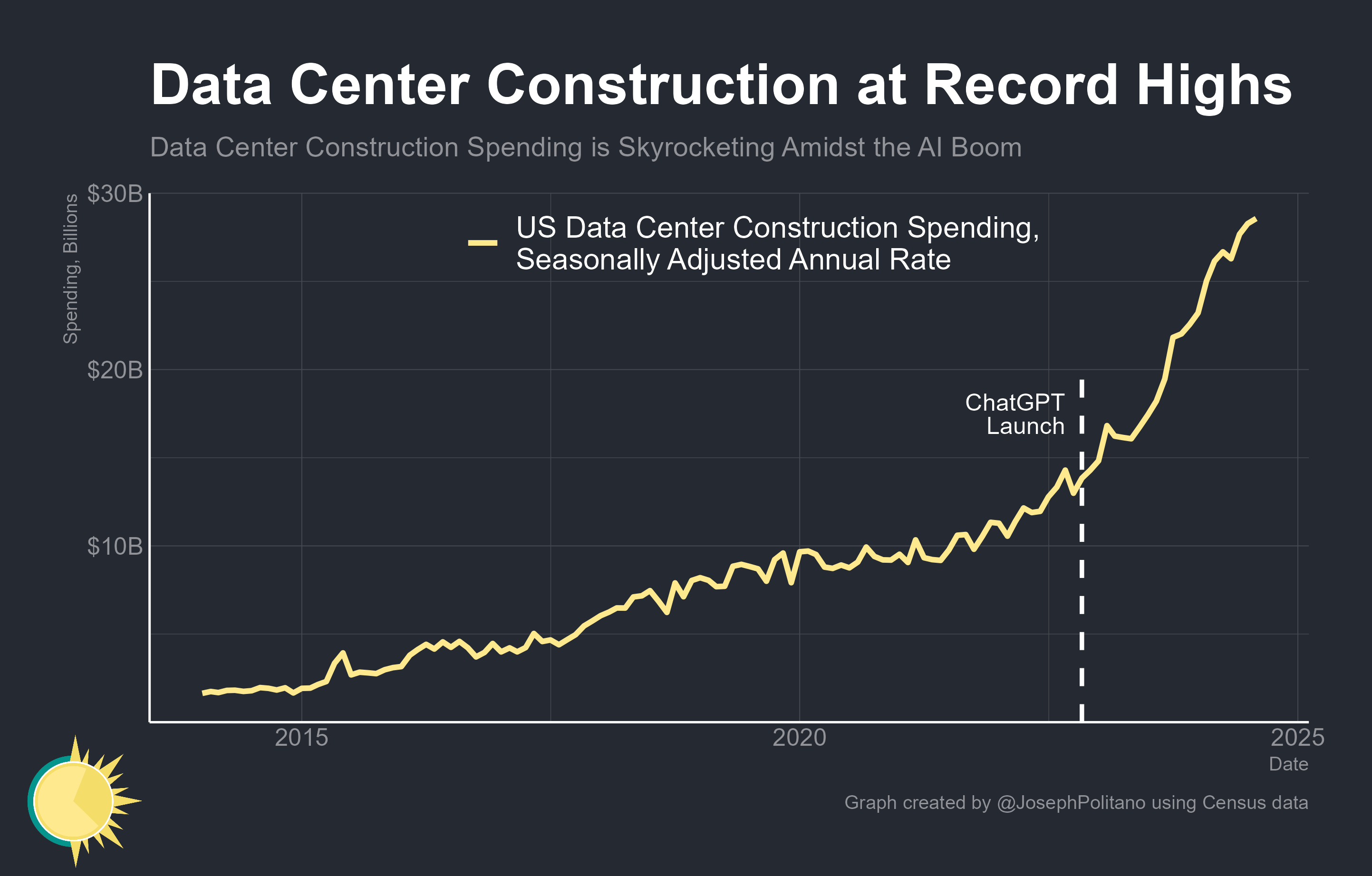

As a result, data center construction hit record levels in the U.S.

These companies are gearing up to handle massive demand expected in 2025.

➔ When all major U.S. companies go all-in on AI, it’s not a coincidence.

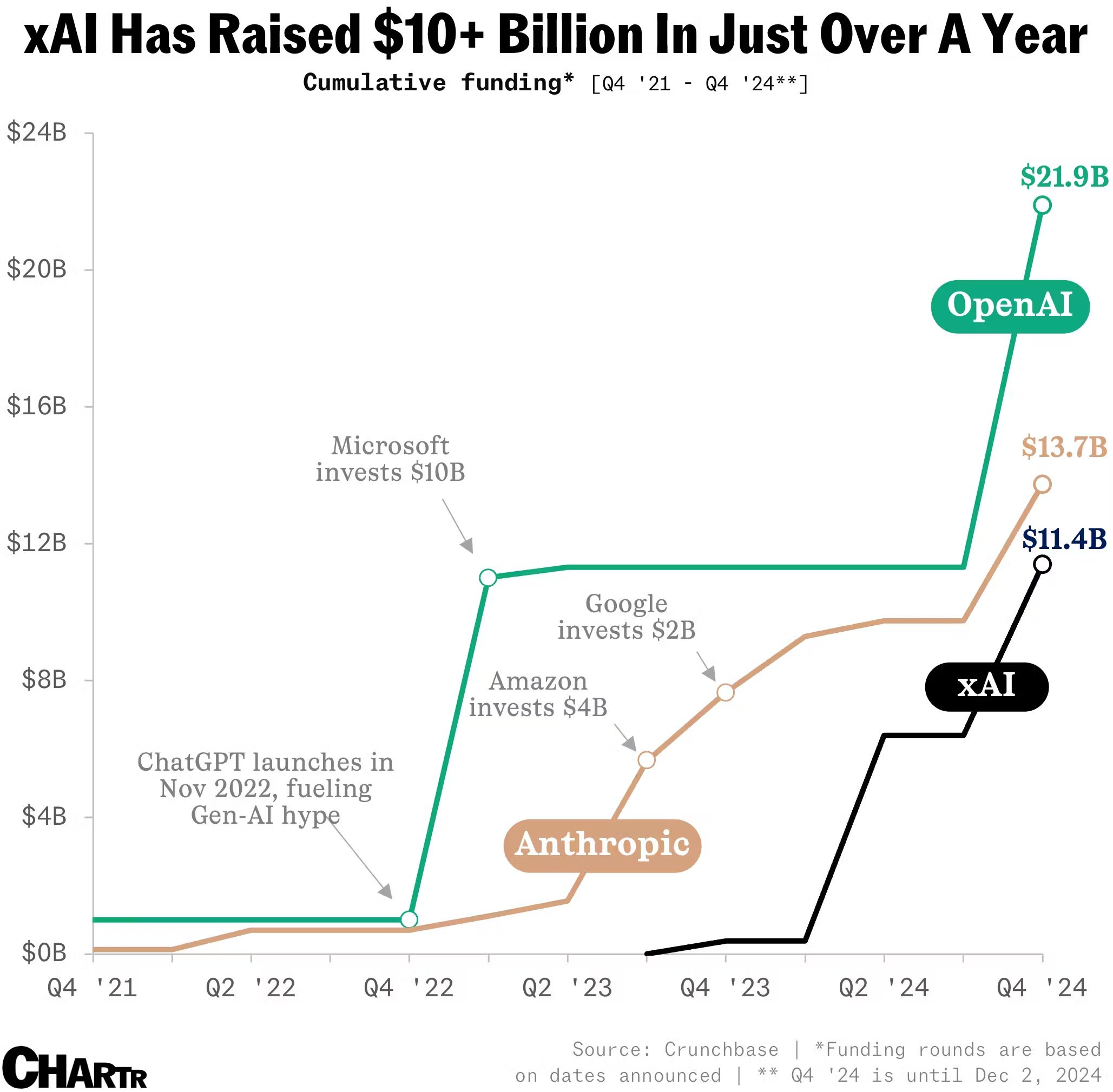

Some are also catching up — like Elon Musk with xAI.

Since July 2023 (just 16 months ago), xAI raised over $11B, something OpenAI took 8 years and Anthropic nearly 4 years to achieve.

xAI is already valued at $50B, more than:

➔ This kind of funding power is rare.

Palantir’s CEO recently made waves, saying: “The AI revolution is an American revolution.”

That’s harsh — but undeniably, the U.S. dominates the global AI scene.

We’ve seen how U.S. giants invest heavily. Their innovation culture fuels this momentum.

Europe is lagging.

Sadly, the investment gap is real: U.S. funding in AI is 10x that of Europe.

Worse, European regulations often hinder innovation:

Regulation often arrives before the tech is mature, putting Europe at a disadvantage.

And with no shared AI strategy, plus heavy bureaucracy, Europe’s position weakens even further.

➔ There's a clear risk of tech dependency on U.S. models, and a loss of industrial sovereignty.

China is better positioned to compete with the U.S., thanks to:

China also publishes more AI research papers than Europe.

In 2024, AI assistants became true productivity boosters, helping us — not replacing us.

Microsoft coined the “copilot” concept.

Its CEO emphasizes that AI supports employees by automating repetitive tasks, without replacing them.

Each AI model now lets users create custom versions to carry out specific tasks via instructions.

➔ OpenAI’s “GPTs” launched in November 2023.

Many users now have their own — and if not, I made a video to help.

➔ Claude calls them Projects

➔ Gemini calls them Gems

Different names, same idea.

But these tools still lack true autonomy.

Still, it’s a strong first step — non-technical users can now automate increasingly complex tasks.

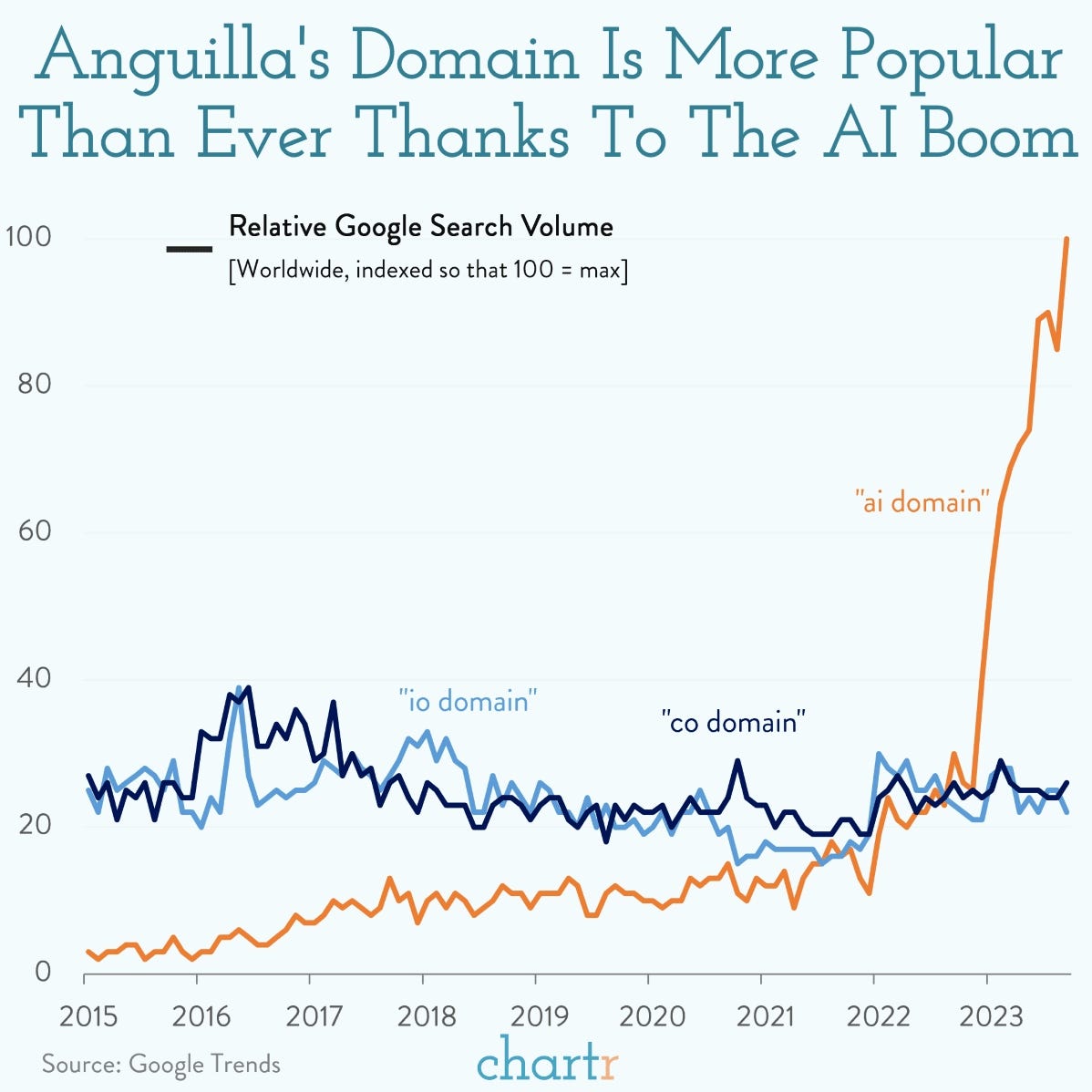

A surprising winner from the AI boom: Anguilla, a tiny island nation.

Thanks to its .ai domain extension, Anguilla now earns $3M/month from domain registrations.

Most short and catchy .com domains are taken — so .ai is booming.

A surprising stat worth sharing.